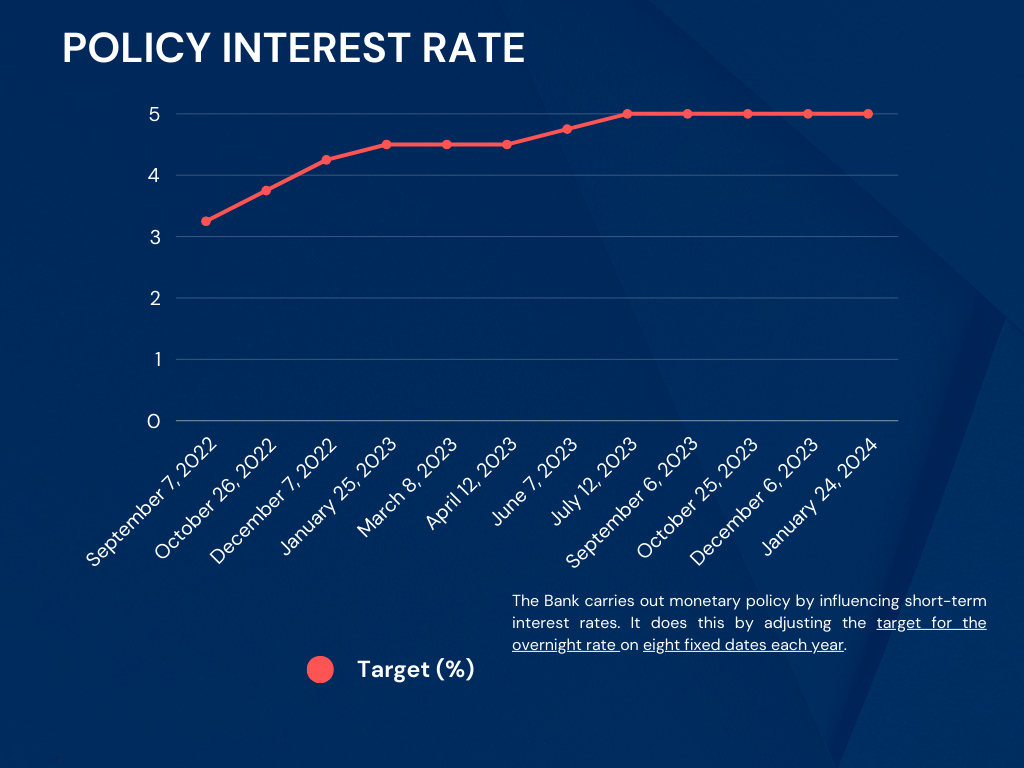

The Bank of Canada kept its trendsetting interest rate at rock-bottom levels on Wednesday, holding off on planned increases aimed at controlling surging inflation.The central bank’s overnight rate remains at 0.25%, a rate it adopted in a drastic drop in the early days of the COVID-19 pandemic.The move is in keeping with the signal from the Bank of Canada late last year that it would begin to hike interest rates toward the middle of 2022. However, some economists predicted officials would move earlier in an effort to cut off surging inflation on housing and other consumer goods.

How the numbers impact a variable rate mortgage

Let’s look at a hypothetical scenario. For those considering locking in their mortgage, assuming a current rate of 1.45% is an adjustable rate which will fluctuate with prime. If we were to consider locking in your rate, it would lock in closer to 2.7% to 2.9% for a 5 year fixed term. This would not only increase your interest rate but also the amount of interest you are paying per installment as well as your total payment. If the rates were to increase, it would most likely be (based on historical trends) by a quarter point. This would bring your interest rate to 1.7%, which is still much lower than the fixed rates that are currently being offered.If you are concerned about your payments increasing, we may have the ability to adjust your payment frequency. We are monitoring interest rate decisions from the Bank of Canada and will keep you posted on any changes. I am happy to discuss if you have any questions or concerns.